2. On Bretton Woods

Stuart Holland

We reprint this excerpt from Stuart Holland's book Towards a New Bretton Woods: Alternatives for the Global Economy (Spokesman Books, 1994).

Keynes' major contribution in The General Theory (1) in 1936 had been on the demand side of national economic policy. As he put it in his Concluding Notes [chapter 24]: provided the state intervened to manage the level of demand, the processes of perfect and imperfect competition would by and large take care of what was produced, in what way and on what scale, as well as 'how the value of the final product would be distributed'.

The contribution of Keynes at Bretton Woods reflected his reasoning in a paper which had been published in April 1943, and whose plan was the following.

We need an instrument of international currency having general acceptability between nations, so that blocked balances and bilateral clearings are unnecessary …

We need an orderly and agreed method of determining the relative exchange values of national currency units, so that unilateral action and competitive exchange depreciations are prevented.

We need a quantum of international currency, which is neither determined in an unpredictable and irrelevant manner as, for example, by the technical progress of the gold industry, nor subject to large variations depending on the gold reserve policies of individual countries; but is governed by the actual current requirements of world commerce, and is also capable of deliberate expansion and contraction to offset deflationary and inflationary tendencies in effective world demand.

We need a system possessed of an internal stabilising mechanism by which pressure is exercised on any country whose balance of payments with the rest of the world is departing from equilibrium in either direction, so as to prevent movements which must create for its neighbours an equal but opposite want of balance.

We need an agreed plan for starting off every country after the war with a stock of reserves appropriate to its importance in world commerce, so that without undue anxiety it can set its house in order during the transitional period to full peace-time conditions.

We need a central institution, of a purely technical and non-political character, to aid and support other international institutions concerned with the planning and regulation of the world's economic life.

More generally, we need a means of reassurance to a troubled world, by which any country whose own affairs are conducted with due prudence is relieved of anxiety for causes which are not of its own making, concerning its ability to meet its international liabilities; and which will, therefore, make unnecessary those methods of restriction and discrimination which countries have adopted hitherto, not on their merits, but as measures of self-protection from disruptive outside forces.

Bretton Woods and after

The establishment of the International Monetary Fund (IMF) and the International Bank for Reconstruction and Development (the World Bank) was influenced by Keynes, but in practice dominated by the United States and its prevailing economic orthodoxies. Both institutions were the outcome of the conference at Bretton Woods in New Hampshire in 1944 to agree on a system of international payments for the post-war period, and which included representatives of the key countries that had taken part in the alliance against Germany, Italy and Japan.

Keynes himself later said that the International Monetary Fund ought to be called a bank and the World Bank should be called a fund. This name game was to be reflected in a constrained role for the World Bank in the later post-war period. In terms of the Bretton Woods objectives, the IMF was supposed to deal with short-term foreign-exchange and balance-ofpayments problems. The World Bank was scheduled not for project finance but for the more ambitious aim of global development.

On the trade and payments front, Keynes was concerned that the key lessons should be learned from the crises of the 1930s. In his view, a system of floating exchange rates could lead to disaster in international economic affairs.

One of the vital roles of the Fund in what might be called the 'post Keynesian' period of its operation, was to achieve an ordered system for exchange-rate changes. It was anticipated that such changes would be made only in the face of serious and persistent disequilibria in the balance of payments of individual countries, and only after consultation with the IMF. IMF lending to an individual country would be conditional on evaluation of the viability of a particular exchange rate.

By contrast with this short-term interventionist role anticipated for the IMF, the International Bank for Reconstruction and Development, or World Bank, was designed to facilitate long-term capital movements. With funds of its own, the Bank can in principle lend to countries in need for development purposes – but also like the IMF – its lending gives 'a seal of approval' which legitimates additional private bank spending in such countries.

In practice – and contrary to widespread public perception – Keynes did not in fact gain his basis for a new international economic order at Bretton Woods. Sir Roy Harrod (2) has chronicled Keynes' exchanges with his formal antagonist at the conference – US representative Harry White. But Keynes' real antagonist was the profound conservatism of a US establishment much less convinced than an already ailing President Roosevelt that the Bretton Woods system would establish a global New Deal.

Keynes had been ambitious for the IMF. He wanted it to overcome the preoccupation with available savings to finance investment, and instead provide sufficient finance to meet increased demand with increased investment and output. The issue as to whether one has the money today to finance investment or whether one should create credit instruments to increase investment, jobs and income has been one of the ongoing differences between Keynesians and monetarists through the 1970s and 1980s.

Such analytic differences about the role of public borrowing became subsumed at Bretton Woods into how big the new IMF's lending facilities should be. Keynes envisaged an IMF scheme involving funds some five times those advocated by White. In practice the final act of Bretton Woods contained a compromise figure much closer to the White recommendations than to those of Keynes. As Harrod (1963, p.549) stressed: Keynes wanted a fund so large as to give governments the confidence necessary to relax unneighbourly restriction; $25 billion might have achieved that (the Keynes plan); $5 billion (the White plan) certainly would not. Was this Fund really to be the foundation for the building of a better world? Or was it to be merely a modest subscription towards meeting some of the needs of poorer countries? Contemporary and subsequent opinions outside the United States have on the whole agreed in holding that Keynes was right.

One could only console oneself by hoping that, should the Americans prove obdurate now, the Fund might be enlarged in the course of its operation.

Allowing for the facility introduced since the late 1970s (whereby central banks can exchange unwanted dollars for Special Drawing Rights or SDRs), Keynes' proposals for IMF quotas, translated into current terms, could have meant a level of official quotas equivalent to between a fifth and a quarter of current trade. As it is, the leading industrial economies at the end of 1984 had reserves excluding gold equal to only the value of some two months' import trade, while the ratio of such reserves to import finance for all the market economies was only some 10 weeks.

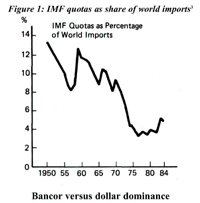

The marginal role of the World Bank can be illustrated by the fact that, by 1985, disbursed resources were equivalent to less than two per cent of global debt. Meanwhile, as illustrated in Figure 1, the IMF quotas which Keynes intended should offset temporary payments deficits and avoid domestic deflation had shrunk from an eighth to less than a twentieth of world import trade between 1950 and 1975, i.e. at the time when they were needed to provide an alternative to the devalued dollar and to beggar-myneighbour deflation by the OECD countries.

Bancor versus dollar dominance

Keynes wanted to see potential world demand matched by an expanding international currency unit which would not need to be fully backed either by gold or national currencies: Bancor. But, in reality, international trade and payments in the post-war period up to the early 1970s was dominated by the United States dollar. So long as the dollar was strong and stable, it played a primary global role, while the IMF and World Bank were upstaged minor actors. But within a quarter of a century of the Bretton Woods settlement, with its much weakened version of Keynes' own proposals, the dollar itself was under major pressure.

One of the main reasons was the recovery of Europe and Japan and the decline of US dominance. Thus while the United States in 1950 had accounted for more than half of the output of what now are the OECD countries, by 1973 this had declined to less than two-fifths.(4) The US share of world trade including the centrally planned economies had declined from about 17 per cent to 12 per cent over the same period. More strikingly, US gold reserves had fallen from nearly 70 per cent to under 30 per cent of the world total from 1950 to 1973, and to less than a quarter by 1984.

Moreover, the new post-war competitors to the United States – most notably West Germany and Japan – had managed to achieve levels of innovation, productivity and competitiveness which had already pushed the US government onto the trade defensive by the mid 1960s.

Throughout the post-war period, the United States allowed or encouraged the export of capital and direct investment on a global scale. But this tended to substitute direct foreign production for export trade, and considerably undermined US visible export performance. The emerging US dollar deficit gave rise to a market for dollars mainly managed in Europe, and soon identified as the 'Eurodollar' market, lying outside the control of the US Treasury. Meanwhile, the US trade deficit, aggravated by the Vietnam War, resulted in major pressure on the dollar and its devaluation under the Nixon administration in 1971.

Had Keynes been able to create a genuinely international reserve currency such is Bancor, the devaluation of the dollar might not of itself have resulted in the collapse of the exchange rate framework of the original Bretton Woods system. But dollar devaluation meant a significant decrease in the value of (dollar-denominated) revenues for the petroleum-producing countries, which anyway had suffered a decline in the real value of their dollar earnings per barrel of oil in preceding years. They hit back by forming OPEC. In response, as already indicated, the developed countries cut civilian public expenditure.

Such 'beggar-my-neighbour' deflation was aggravated by the re-emergence of the pre-Keynesian orthodoxy of 'sound money supply', validated in the eyes of many treasuries, chancelleries and central banks by the work of Milton Friedman and his associates. Thus, although Keynes had never wanted the dollar to be the last resort and the lynchpin of the international monetary system, combined with inflationary tendencies from the mid 1960s, this represented a profound challenge to the viability of so-called Keynesian policies in the international economy.

Footnotes

1. Keynes, J.M., (1936) The General Theory of Employment, Interest and Money, Macmillan. London.

2. Harrod, R.F., The Life of John Maynard Keynes, Macmillan, London, 1963.

3. Source: IMF and The Economist.

4. The increase in the US share of OECD output by 1984 reflected both the sustained expansion of the American economy and the restraint on growth in the other principal OECD economies. In contrast with the low share of the US in world total exports in 1984, US imports were 19 per cent of the world total, reflecting the vast trade deficit which accompanied the US 'boom'.